Do you also have the same question, what is digital payment? We know that until a few years ago, many people felt unsafe if they did not have cash in their pockets. If you wanted to buy something from a shop, you had to find an ATM first. But now the situation has completely changed.

Today, while having tea, buying vegetables, shopping online or sending money to a friend, we just take out our mobile, scan the QR code and the payment is completed in a few seconds.

Digital Payments have created a huge revolution in India in the last few years. Transactions have become faster, safer and easier due to UPI, Mobile Banking, Wallets and Contactless Payments.

In this article, we will learn in detail about what is Digital Payment, how it works, its types, advantages, disadvantages, security tips and the future of Digital Payment in India.

Quick Takeaways

- Digital Payment means transferring money electronically without cash.

- UPI is the most popular digital payment system in India.

- QR Code payments are growing rapidly in rural and urban areas.

- Digital Payments are fast, secure, and convenient.

- OTP and UPI PIN should never be shared with anyone.

- Mobile Banking and UPI have transformed India’s banking system.

What is Digital Payment?

Digital Payment is the transfer of money electronically without using any cash.

Simply put, Digital Payment is the process of sending money from one person’s bank account to another person’s account with the help of mobile, internet or digital systems.

In this transaction:

- No need for cash

- Transaction is processed online

- Money is transferred in seconds

- A digital record of each transaction is created

Today, many methods are used in Digital Payments such as:

- UPI

- Debit Card

- Credit Card

- Mobile Wallet

- Internet Banking

- Mobile Banking

- QR Code Payments

- Contactless Payments

How did Digital Payments start?

Earlier, Banking was based on Bank Branch, Passbook, Cash Counter, Cheque Payment.

After this, ATMs came and people could withdraw money 24×7. Later, Internet Banking started and Online Transactions started increasing.

After Smartphone and Internet became cheaper, Mobile Banking and UPI created a Digital Revolution in India.

Specifically:

- Demonetization

- Cheap Internet

- Government Digital Campaign

- NPCI’s UPI System

Due to this, the use of Digital Payments in India increased tremendously.

Today, India has become one of the largest Real-Time Payment Ecosystems in the world.

How do Digital Payments work?

When you make a payment by scanning a QR code, several processes take place in a few seconds.

1. Payment Initiation

First, the customer initiates the payment. That is, the customer opens the UPI App or scans it and then enters the amount and finally clicks on the pay button

2. Authentication Process

To ensure that the transaction is secure, the customer’s identity is verified.

For this, the UPI PIN is asked while making the transaction, then OTP, password fingerprint and face unlock are used for security.

3. Data Encryption

To keep the customer’s banking information safe, the information is encrypted. This reduces the risk of hacking, fraud is prevented, and the data remains secure.

4. Payment Processor and Gateway

The Payment Gateway delivers the transaction information to the bank and the Payment Network. Is the System Account Valid?, Is there money in the account?, Is the transaction safe? All these things are checked.

5. Bank Verification

The customer’s bank approves or rejects the transaction.

If there is enough money in the account, the Payment is Approved. And if there is no money in the account, the bank declines the transaction.

6. Funds Transfer

After this, the money is transferred from the customer’s account to the merchant’s account. This process is often completed in a few seconds. This requires good internet. If the internet speed is high, the transaction is completed in a few moments and if the internet speed is low, the transaction takes some time.

7. Confirmation Message

After the transaction is completed, the customer receives a confirmation message, or an app notification or a payment success message.

Who is involved in the Digital Payment System?

There are many organizations working behind a simple payment.

1. Customer

A customer is a person who is going to make a payment to another. For example, when you buy an item, you transfer money to that person online to pay for that item, in this situation you are a customer.

2. Merchant

Just as the person making the payment is called a customer, the person or organization who is going to receive the payment or the person or organization to whom the money is going to be received is called a merchant. The person receiving the payment can be a shopkeeper or a business.

3. Issuer Bank

The bank in which the customer’s account is located is the Issuer Bank. This bank checks the balance on its customer’s account and completes the transaction only if there is a balance and declines the transaction if there is no balance in the account.

4. Acquirer Bank

The bank in which the merchant’s account is located is the Acquirer Bank. That is, the bank in which the customer transfers money to the account of the person to whom the account is located is called the Acquirer Bank.

5. Payment Gateway

A system that processes transactions securely is called a payment gateway.

6. Payment Network

Money is transferred from one person to another through institutions like UPI, Visa, RuPay, Mastercard, which route transactions. These are called payment networks.

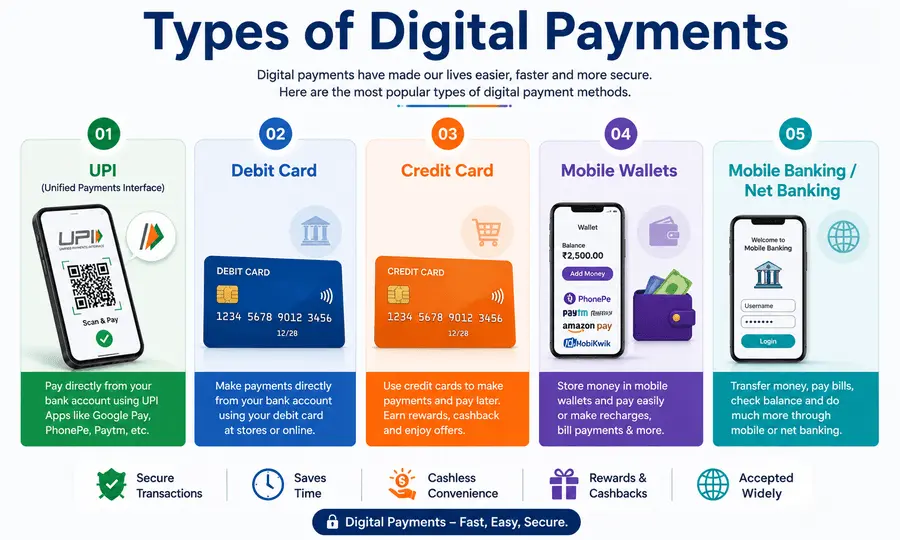

Types of Digital Payment

1. UPI Payments

UPI stands for Unified Payments Interface. This is the most popular digital payment system in India.

Instant Money Transfer can be done with the help of Mobile Number, UPI ID, QR Code.

Example:

- Google Pay

- PhonePe

- Paytm

- BHIM UPI

2. Mobile Wallets

Mobile Wallet is a digital wallet in which money can be stored and transacted.

Example:

- Paytm Wallet

- Amazon Pay

- Mobikwik

With the help of this wallet, a person can store his money and transfer it to another person.

3. Debit Card Payments

A Debit Card is directly linked to a bank account.

When you use the card, the money is deducted directly from the account.

If you want detailed information about what a debit card is, you can read our article: What is a Debit Card? Meaning, Benefits and How It Works

4. Credit Card Payments

In a credit card, the bank allows you to use borrowed money up to a certain limit. But interest may be charged on the amount used through the credit card. Check the terms and conditions of the credit card before using the credit card.

5. Internet Banking

The facility to make online transactions using the bank website is Internet Banking. For this, the bank provides you with the facility of login ID and password. The login ID is called customer ID here. With the help of that customer ID and password, you can handle the facility of internet banking.

These include services like:

- NEFT

- RTGS

- IMPS

6. Mobile Banking

With the help of the bank app, you can transfer funds, make bill payments, check balance, and if you want to make investments, you can do it too. All these things are done through the bank app through mobile, which is called mobile banking.

7. AEPS

In the Aadhaar Enabled Payment System, transactions are made using Aadhaar and Fingerprint. This method is probably not used much.

8. USSD Banking

Even without internet, the bank provides its customers with the facility of making banking transactions through *99#. You do not need internet for this.

9. QR Code Payments

QR code payment is considered as a modern method of making instant payment by scanning QR. Here you just have to scan the QR code, then enter the amount and make the payment.

10. Contactless Payments

The facility of making payment by tapping the card is known as Contactless Payment. Here you just have to tap the card and then the payment automatically goes to the next merchant.

Popular Digital Payment Apps in India

1. Google Pay

Google Pay is considered a very popular app due to its simple interface and fast UPI transactions. It is a product of Google.

2. PhonePe

It is widely used for Recharge, Bills, Insurance and UPI Payments. Like Google Pay, PhonePe also offers many facilities to its customers.

3. Paytm

Paytm is an app that offers Wallet + UPI + Banking facilities. After Google Pay and PhonePe, Paytm is the most used customer.

4. Amazon Pay

Amazon Pay is a product of Amazon. This application will be useful for you for Online Shopping Payments. After you buy a product online, Amazon Pay is used to make payment there.

5. BHIM UPI

BHIM UPI is the Official UPI App created by NPCI. There are also a large number of customers who use this app.

Benefits of Digital Payments

1. Fast Transactions

The biggest advantage of digital payments is that we can complete our transactions in a few seconds. That is, we can transfer our money to another person in a very short time.

2. Convenience

Another important advantage of digital payments is that we do not need to carry cash in our pocket. Because we send money from one person to another online.

3. Better Security

The third important advantage of digital payments is that transactions are done online, so security is very important here. To complete every transaction, we have to use OTP, PIN and encryption makes transactions secure.

4. Transaction Record

While making a diesel payment, the platform or app from which you are making a digital payment has all your previous transactions in your country in the history of the app, so the history of all transactions is available.

5. Cashback and Rewards

Some apps give you many App Offers and Cashback based on your digital payment i.e. online payment. Coupon codes are given. Which we can use during other transactions.

6. Business Growth

Accepting Digital Payments increases customers. Due to this, the business also grows. Because customers increase, when customers increase, payments increase, and then when payments increase, the income model and the benefit of that income will be for business growth.

7. Financial Inclusion

Initially, financial awareness was high only in urban areas, but now people in rural areas are also using digital payments a lot, so we see financial inclusion here too. People in rural areas also get banking facilities.

8. Global Transactions

An important advantage of using digital payments is that we can transfer money for transactions outside the country even from home, which means that now it has become easier to make international payments.

Benefits of Digital Payments for Businesses

1. Better Cash Flow

There are also important benefits of digital payments for businesses such as the money is immediately credited to the account of the next merchant.

2. Easy Accounting

Since all the history of digital payments is available, a digital record of all transactions is available. Therefore, accounting is done in an easy way for every business organization.

3. Customer Satisfaction

Digital payments are very important for the goodwill of a business because fast checkout is done through digital payments and this keeps the customers happy. The reputation of the business increases.

4. Sales Analysis

Due to digital payments, a business organization can see how much sales its business has done or sales analysis according to its complete history, i.e. the business understands Customer Behavior. Therefore, this is also an advantage of digital payments.

5. International Reach

Whether your business is domestic or international, digital payments help your business in the best way. Due to digital payments, now a business organization can do its business anywhere at the international level because digital payments can accept payments from customers around the world.

Disadvantages of Digital Payments

Although Digital Payments are beneficial, there are some risks as well.

1. Internet Dependency

The most important thing to make digital payments is to have internet. If there is no internet, the transaction can get stuck.

2. Cyber Fraud

Since all transactions are done online, Fake Calls, Scam Links and OTP Fraud are increasing here. Therefore, the chances of cyber fraud are high.

3. Server Issues

Sometimes, Banking Servers are down from the receiver bank or the central bank. Due to this, there may be problems in completing the transaction.

4. Technical Knowledge

Not all people are educated and some people still do not know how to make digital payments, so some people still find it difficult to use Digital Payments.

How to keep Digital Payment secure?

1. Do not tell OTP to anyone

The most important thing to keep digital payment secure is to not tell the OTP that comes while making a payment to anyone.

2. Do not share UPI PIN

Do not share the UPI PIN for the digital payment app in your mobile with anyone. If you share the UPI PIN with anyone, your mobile can be stolen based on that picture and money can be transferred to another account.

3. Do not click on Fake Links

Some links in the mail or text messages that you frequently receive are fake links, so we should all be careful not to click on those fake links. Sometimes, clicking on fake links can leak your information and lead to cybercrime.

4. Avoid Banking on Public WiFi

If there is no mobile internet, you have to use Wi-Fi, but remember one important thing while using WiFi that is, avoid public WiFi while doing banking transactions. Because public WiFi can make your information public and cyber fraud can occur.

5. Use Official Apps

For digital payments, use only government authorized official apps. Or use official apps launched by official organizations. Such as Google Pay, Phone Pay, BHIM, Paytm, Amazon Pay etc.

6. Use Biometric Lock

Use biometric lock instead of using number lock for diesel payments. Because your password can be stolen but biometric is on your therm impression or finger impression. Therefore, using biometric lock will be more secure.

Relationship between Digital Payments and Mobile Banking

Today, Mobile Banking has become the main center of Digital Payment.

Due to Bank Apps:

- Instant Transfers happen.

- Bill Payments can be made.

- Online Investments can also be made.

- Banking Services are also available.

All the above facilities are available on mobile. This has made Banking smarter and easier.

Digital Payment Statistics in India

Digital transactions have seen a huge growth in India in the last few years. Thanks to UPI, QR Code and Mobile Banking, online transactions have become a part of the daily life of the common man. The following are some important statistics that give a clear picture of the growth of Digital Payment in India.

| Statistics Topic | Data / Observation |

|---|---|

| Monthly UPI Transactions | India records more than 15 billion UPI transactions every month |

| India’s Global Position | India is one of the world’s largest real-time payment markets |

| QR Code Usage | QR Code payments are rapidly growing in rural and urban areas |

| Mobile Banking Growth | Mobile Banking users are increasing rapidly due to smartphones and cheap internet |

| Cashless Economy Trend | India is moving quickly towards a cashless economy after Digital India initiatives |

| Small Business Adoption | Small businesses now accept most payments through UPI and QR Codes |

| Online Bill Payments | Millions of users pay electricity bills, recharge, and shop online using digital payments |

| Security Awareness | OTP verification and biometric security are making online payments safer |

I myself have seen a big change in the last few years — earlier, digital payments were mostly used only in big cities, but now QR Code payments are easily accepted in small shops in villages, vegetable markets, and even tea stalls.

Why are Digital Payments so Popular in India?

There are many reasons behind the growth of Digital Payments in India. Such as

- Availability of cheap internet.

- Smartphone usage is increasing.

- UPI Revolution has taken place.

- QR Payments facility is also available

- Cashback Offers are also available.

- Government Support is also available

Today, from small village shopkeepers to large companies, everyone is accepting Digital Payments.

Future of Digital Payments in India

Digital Payments will be further advanced in the future.

These include:

- AI Payments can come in the future.

- Voice Payments can also come in the future.

- Biometric Transactions can happen.

- Digital Rupee can come.

- Wearable Payments can be available.

- The use of such technologies will increase.

India is rapidly moving towards a Cashless Economy.

Important Facts about Digital Payments

- India is one of the largest UPI Ecosystems in the world

- Billions of UPI Transactions are done every month

- QR Payments are also growing rapidly in rural areas

- The number of mobile banking users is constantly increasing

Frequently Asked Questions (FAQ) : What is Digital Payment

What is Digital Payment?

Digital Payment is the transfer of money electronically.

What is the difference between UPI and Wallet?

UPI is directly linked to a bank account, so you have to add money to the Wallet first.

Is Digital Payment safe?

Yes, Digital Payments are safe if proper security measures are used.

What is the most popular Digital Payment Method in India?

UPI is the most popular Payment System in India.

How does QR Code Payment work?

After scanning the QR, the payment process is done through the UPI App.

What is the difference between Mobile Banking and Internet Banking?

Internet Banking runs on a website, while Mobile Banking is used through an App.

Conclusion

Digital Payments have made financial transactions faster, safer and more convenient today. UPI, Mobile Banking and QR Payments have ushered in a Cashless Economy in India. However, it is equally important to follow safety rules while using Digital Payments. With proper awareness and safe use, Digital Payments can be the most powerful financial system of the future.

If you are not yet using digital payments, start with small transactions today. With the right information and secure methods, digital payments can make your life easier, faster, and safer. If you found this article helpful, be sure to share it with your friends and family.

Disclosure

This article is written for educational and informational purposes. The information in the article is based on personal experience, research, public sources and general usage of digital payment services. Please consult your bank, official website or financial expert before making any financial, banking or investment decisions.

The UPI Apps, banks or digital services mentioned in the article are only examples. We do not officially represent any particular company. Always follow security rules while making digital transactions and do not share OTP, PIN or personal bank details with anyone.

Hello! I’m Abhijeet Bendale, founder of MoneyPedia (Your Trusted Banking Guide). With 8 years of experience in the education field, I aim to simplify banking and personal finance topics for everyday readers through easy-to-understand guides and tutorials.

At MoneyPedia, I share informative content on UPI, digital payments, net banking, ATM and debit cards, mobile banking, and other essential banking topics to help users make smarter financial decisions with confidence.